User Owned Platforms

“The three most harmful addictions are heroin, carbohydrates, and a monthly salary.”

- Nassim Taleb

Ben Thompson wrote an interesting post recently on the topic of Substack, highlighting its opportunity and challenges. I highly recommend that you read it. Beyond being a good take on Substack, it makes the case, albeit unintentionally, for a larger trend we are already seeing, and will continue to see across platform businesses: the proliferation of user-owned platforms.

Substack: a platform to elevate individual writers

Before delving into the discussion around user-owned platforms, lets take a quick look at a Substack. Substack is a platform that gives writers the ability to monetize their audience directly and the opportunity to be compensated appropriately for their work. Writers can spin up their own publication through Substack without having to ply their trade within the confines of a larger organization.

Readers can subscribe to individual writers that they want to follow, and pay them directly. While Substack levies a 10% fee on the revenue writers generate and Stripe takes a small cut for processing the payments, the amount of middlemen involved in the communication between writers and their audience is sharply reduced. Writers talk directly to their readers and create content exclusively for them.

Substack has given writers a platform that enables them to become more than just employees, but founders of their own media conglomerates. While the core feature is a newsletter, Substack also allows writers to record podcasts and will likely expand into additional mediums in the future.

The platform tension: value creation vs. value extraction

With this in mind, as with every platform, there exists a constant tension between value creation and value extraction. Substack is no exception to this. Virtually all the large platforms of today started off by initially focusing on value creation for their users and enabling them to succeed. Once users were successful and dependent on the platform, platforms could then leverage that lock-in effect to maximize value extraction from their users.

However, Substack is different to a lot of other platforms, in that it lacks some critical levers for creating a strong lock-in. Ben Thompson explains in his post:

“Substack does an excellent job helping publishers get started; what concerns me as an analyst is how they avoid losing folks out the top. Suppose a publisher is earning $1 million in revenue a year: at what point does that publisher start to wonder if Substack’s $100,000 take is worth it? Unfortunately for Substack, that publisher owns their readers; note the bit above about Stripe fees being separate from Substack fees, which also means that readers — and their credit cards! — exist in that publisher’s Stripe account, along with their email addresses. If anything, this makes hysterical proclamations that Substack is some kind of nefarious new platform deeply ironic: Substack’s entire problem from a business perspective is that it failed to implement the exact sort of platform lock-in that folks are worried about.”

Just last week we saw what can happen when writers feel that they have outgrown the platform, with two widely read newsletters, The Generalist and Every.to, being taken off Substack by their creators onto their own stacks.

Crucial to Substack's model is not only the ability to acquire writers, but to grow with them. If writers think that the 10% take rate that Substack levies is too much, they can take the audience they have built on Substack and continue to run their business elsewhere. They own their mailing list and the content doesn't actually need to be consumed on the Substack platform. Newsletters land in readers' inboxes and can be consumed there. It turns out that Substack's lack of levers for lock-in is great for the writer, but not great for the Substack business itself.

User-owned platforms align incentives

The open design of platforms is not something that needs to be bad for business, however. Rather, what an open platform needs is a new ownership model: a platform that is owned by its users.

Taking Substack as an example, in such a scenario, writers wouldn't only be users of the platform and pay a tax on their revenues, but co-owners of it. This creates a greater alignment between value creation and value capture, as the people that provide value to the platform, the writers, are also the ones that extract it. If writers got so big to a point they would consider leaving the platform, they wouldn't, or at the least think harder about doing so. Their success contributes to the success of the platform, which they are owners of.

The ensuing question that naturally follows is what user owned platforms look like in practice. As it turns out, we already have live and functioning examples in the wild. One of the most compelling resides in the arena of decentralised networks and crypto-assets. It's called Uniswap.

Uniswap: an exchange platform owned by its users

Uniswap is a decentralized exchange that's built on Ethereum. It's an alternative to centralized exchanges like Coinbase or Binance, where users can go to trade their tokens. The exchange has seen substantial volumes over the last couple months, even outperforming its centralized peers at times.

The exchange's liquidity is provided by its users. Uniswap allows anybody with a balance that's greater than zero to be a liquidity provider for specific token pairs. As an example, if you want to be a liquidity provider for the ETH / MKR pair, you need to provide an equal USD denominated amount in both tokens. Once users have provided liquidity to the pool, they get trading fees proportional to the percentage of the total liquidity they've provided. If someone has provided 10% of the liquidity for that specific pair, they get 10% of the fees.

While there are certainly a large degree of differences in exchange mechanics and in the underlying technology between Uniswap and exchanges such as Coinbase, the defining difference is in their ownership structures. Coinbase is owned exclusively by its founders, investors and early employees, whereas Uniswap is majority owned by its users.

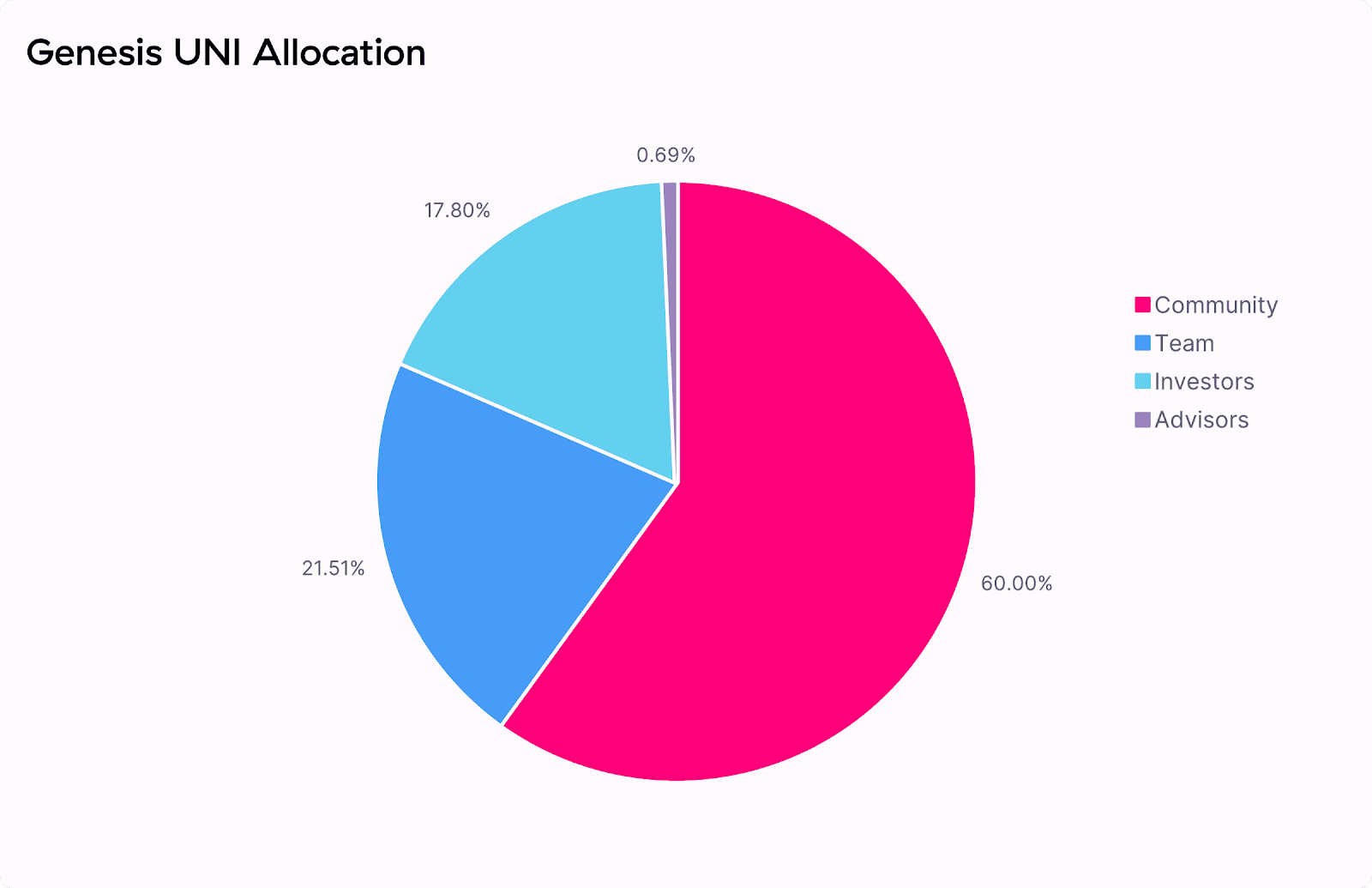

As opposed to distributing equity as a means of splitting ownership, Uniswap distributes its native token, UNI, to its users. When the Uniswap token allocation was initiated in 2020, the platform had already been live for roughly two years. In order to reward the people that had helped the platform function and grow in its early days, Uniswap distributed 15% of the initial token supply (150 million UNI tokens) to users that in the preceding two years had at some point engaged with the platform, either as liquidity providers or users that had simply traded tokens.

At the time of writing, the UNI token price is $22.94. The current market value of the 150 million tokens Uniswap distributed to its users is as a result $3.4B. The value of UNI is derived from the ability to influence the governance of the Uniswap platform, including an anticipated vote that would allow token holders to receive trading fees.

Income complemented with capital appreciation

The important distinction to note is that user-owned platforms create a construct whereby users are owners and as a result generate wealth through both income and capital appreciation.

- Income: revenue generated from providing liquidity. The more liquidity users provide, the more they earn. The more paying subscribers writers have on Substack, the more they earn. People get appropriately rewarded for the value they provide individually to the platform.

- Capital appreciation: token appreciation. As users are also owners of the Uniswap platform they benefit from the collective effort of all the other users, which is reflected in the overall value of the platform. If the platform does well, so too should the token price. This is unique to user owned platforms.

While the majority of Uniswap ownership is given to the community, the team building the actual software and the investors that supported the team early on, also own part of the platform. The incentives between users, the team and investors are aligned as they all own a piece of the same platform. They own the same tokens with the same rights and price. If the team and investors decided to arbitrarily levy unfavorable rules on users, users would leave and take their liquidity elsewhere. A decrease in the value of the platform would ensue, as there would be less trading volume and fees, which would be reflected in a lower token price. In the same vein, decisions that favorably treat users would bring additional liquidity and volumes, which would increase the value of the platform and by extension the token price.

A future where users are owners

The world is waking up to the reality that the platforms of today have become too powerful and value extractive. The platforms of tomorrow will find it more difficult to build sustainable businesses through data monopolisation that keeps users locked in. They will likely be more open and continue to work together with, not against their users.

Parallel to the rising concerns of data monopolies is increasing access to ownership. Companies like Robinhood, Coinbase, StockX, and Otis have played their part in expanding access to ownership over a range of different assets. Buying stocks, shoes, crypto-assets, and fractional shares of art have become part of the mainstream. Accessibility has gone up, as capital requirements have gone down. Democratizing access to ownership is paramount given the historically superior returns on capital over labor.

User owned platforms are an elegant solution that enable both value creation and and more equal opportunity for value capture. By aligning the incentives of users and the builders of platforms, the open nature of platforms is no longer an achilles heel, but a strength.